At a glance

- Typical payoutVaries by case

- Best fitAdvanced cases often qualify

- Tax treatmentOften tax-free under §101(g)

- Timeline30-60 days to funds

- EligibilityPolicy ≥ $100K, 2+ years old

What patients with pancreatic cancer should know

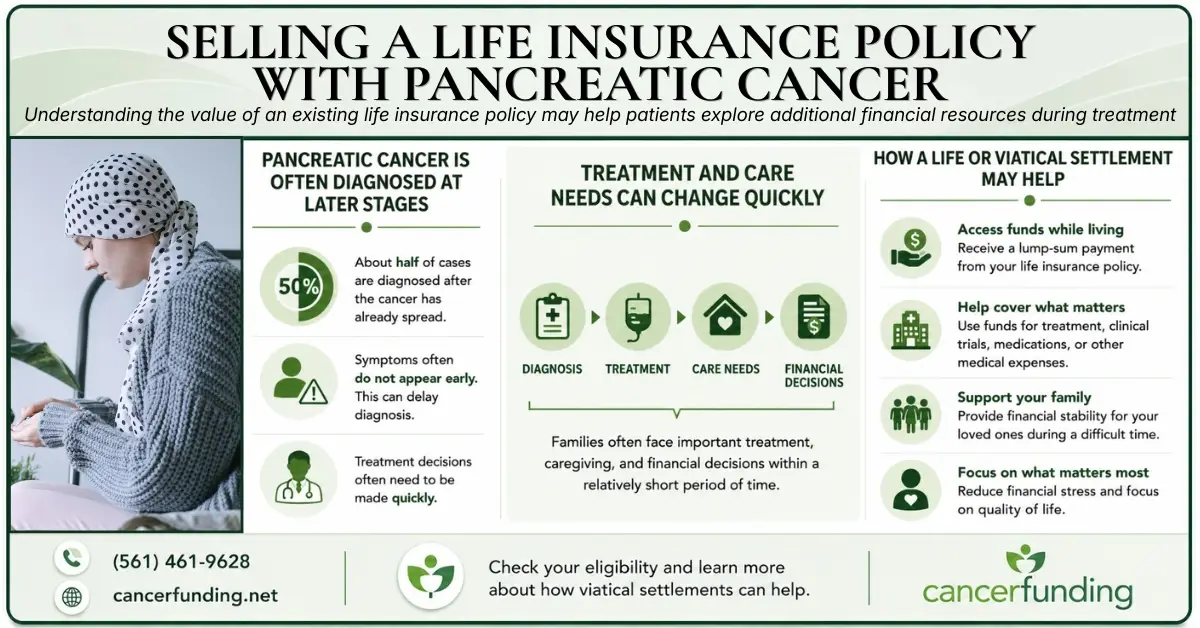

Pancreatic cancer is often diagnosed at later stages — about half of cases are found after the cancer has already spread — and treatment decisions frequently need to be made quickly. Understanding what an existing policy is worth can open additional financial resources during treatment.

A life or viatical settlement lets you access a lump sum while living, which families often use for treatment, clinical trials, medications, and everyday stability. Advanced cases certified by a physician may qualify under IRS §101(g) for proceeds that are generally tax-free at the federal level.

How payout ranges work

Because pancreatic cancer outcomes vary so widely, offers are highly individual — there’s no single percentage that fits every case. The amount depends on diagnosis, stage, prognosis, age, policy type, and carrier. A free, licensed review gives you a specific range, and patients who qualify typically receive substantially more than the policy’s cash surrender value, often delivered within 30-60 days of acceptance.

What we’d recommend asking

- What’s the difference between a life settlement and a viatical settlement for my diagnosis?

- How will this affect my Medicaid eligibility?

- What documentation does the buyer need from my oncologist?

- Is there a rescission window if I change my mind?

- Are there better alternatives (policy loan, accelerated death benefit rider)?