New Hampshire at a glance

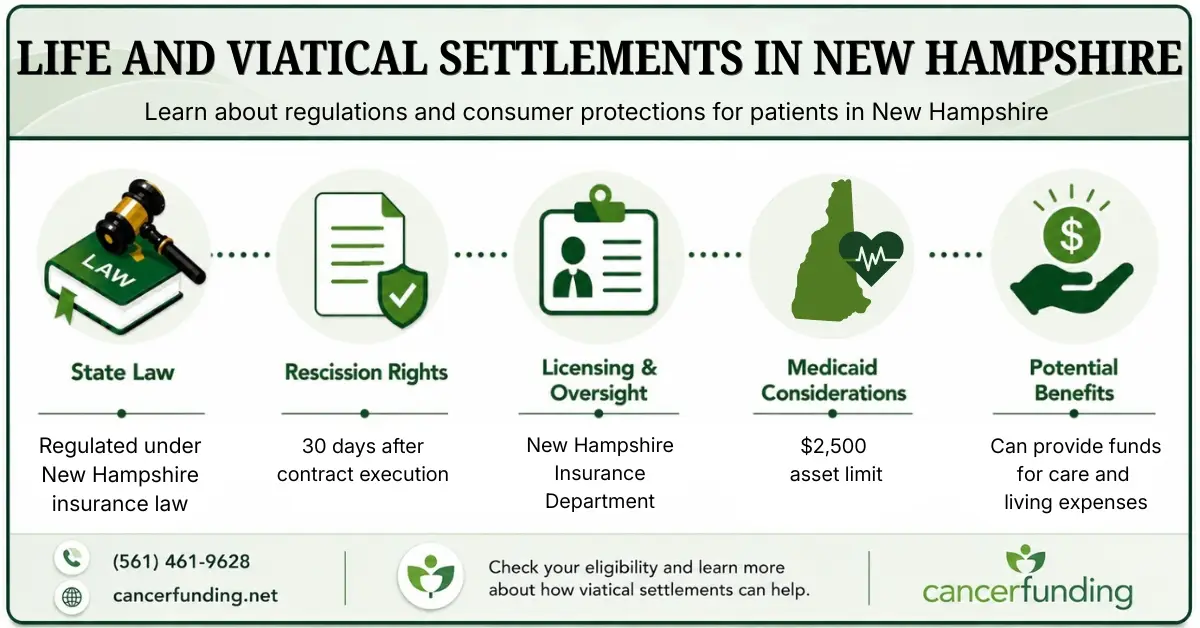

- StatuteRegulated under New Hampshire insurance law (licensing required)

- Rescission window30 days

- Medicaid asset limit$2,500

- RegulatorNew Hampshire Insurance Department

- Licensed providersMultiple

How life settlements work in New Hampshire

New Hampshire regulates life settlement transactions under state insurance law, with licensing required for providers and brokers operating in the state. New Hampshire follows the NAIC Viatical Settlements Model Act's five-year policy waiting period, longer than the two-year period used in most states.

The New Hampshire Insurance Department licenses life settlement providers and brokers and serves as the primary regulatory authority for New Hampshire consumers with insurance-related questions. New Hampshire law gives policy owners the right to rescind a life settlement contract within 30 days after the contract is executed. New Hampshire is also one of six states that requires insurance carriers to tell policyholders about the life settlement option before a policy is allowed to lapse or be surrendered.

For cancer patients in New Hampshire, the most common path is a viatical settlement under IRS §101(g), where proceeds are generally tax-free at the federal level if the insured is certified as terminally or chronically ill. New Hampshire generally follows federal income tax treatment for qualifying viatical settlements.

Medicaid impact in New Hampshire

A life or viatical settlement can affect eligibility for Medicaid and other means-tested public assistance programs. New Hampshire's Medicaid asset limit for individuals is currently $2,500 (2026). Because Medicaid rules vary by program and individual circumstances, New Hampshire residents should review current eligibility requirements through the New Hampshire Medicaid before accepting a settlement.

Depending on your situation, planning tools such as special needs trusts or pooled trusts may help preserve eligibility for certain public benefits. These arrangements generally should be established before settlement proceeds are received.

This is often the most important planning consideration for New Hampshire cancer patients considering a life or viatical settlement. We can help connect you with a New Hampshire elder law attorney if additional guidance is needed.

What’s different about New Hampshire

- New Hampshire regulates life settlements through licensing requirements for providers and brokers

- Owners have a statutory right to rescind a life settlement contract within 30 days of execution

- State oversight rests with the New Hampshire Insurance Department

- Medical and policy information remain protected under HIPAA privacy requirements

- Federal tax-free treatment may apply to qualifying viatical settlements under IRS §101(g)

- Medicaid eligibility may be affected by settlement proceeds depending on the recipient's circumstances

Major New Hampshire cities we serve

Statewide. Our licensed specialists work with policies throughout New Hampshire, including Manchester, Nashua, Concord, Dover, Rochester, and Keene, and surrounding communities. No in-person meetings are required. Documentation, signatures, and notarization can all be completed remotely.